What should carbon tax revenue be used for?

Carbon pricing normally serves two purposes – it helps to mitigate global climate change and it helps to fill government coffers.

The dual purpose of carbon tax

Carbon pricing normally serves two purposes – it helps to mitigate global climate change and it helps to fill government coffers.

The way in which a government allocates carbon tax revenues determines, to a great extent, the public’s acceptance of carbon pricing policy and ultimately the success of this climate mitigation strategy. But how do policy makers choose between the different spending options for carbon tax revenues to keep all parties happy? This is where an easy-to-follow framework with a range of revenue use options can help.

This article is based on a synthesis article titled “A classification framework for carbon tax revenue use” published in the Climate Policy journal. But first, some background.

Putting a price on carbon is regarded as the most cost-effective regulatory approach to reduce greenhouse gas emissions. By the end of 2019, carbon taxes had been implemented in at least 25 jurisdictions as part of the effort to cost-effectively meet the Paris Agreement goals.

This raised an important question: How should governments put this revenue stream to use?

The way in which a government allocates carbon tax revenues determines, to a great extent, the public’s acceptance of carbon pricing policy and ultimately the success of this climate mitigation strategy.

To find out, this study started off by exploring the various uses of carbon tax revenues, and then put forward a simple classification framework of carbon tax revenue usage, with different modalities to cater for various policy design features. This innovative framework also provides policymakers with an overview of options before engaging in more complex policy deliberations.

Modalities for classifying carbon tax revenue use

This article does not advocate how a government should redirect carbon tax revenue. Instead, it offers a framework of options when considering how revenue could be allocated. This classification framework is aimed at providing a better understanding of the interplay between a jurisdiction’s overarching fiscal policy objectives, the attributes that policymakers need to consider when drafting fiscal policies, and the various carbon revenue spending options.

The goal was therefore to distil salient aspects of revenue use into a classification framework that defines and categorises groups based on shared characteristics – a taxonomy of sorts. These categories are: (1) unconstrained versus constrained usage; (2) revenue-neutral versus revenue-raising expenditure; (3) the allocation of revenue based on public preference; and (4) a thematic approach. Let us take a closer look at these characteristics:

Putting a price on carbon is regarded as the most cost-effective regulatory approach to reduce greenhouse gas emissions.

Unconstrained versus constrained use of carbon tax revenue

The Organisation for Economic Co-operation and Development (OECD) in France defines carbon revenue use according to the restrictions placed thereon. Unconstrained revenue becomes part of the general public revenue while constrained revenue is set aside for specific use. There are two types of constraints, namely earmarking (budgeting procedure of designating tax or other revenue for a particular programme or purpose) and political commitments (which are less restrictive).

The OECD analysis showed that almost half (47%) of the examined countries that have a carbon tax in place applied some form of earmarking to the revenues, while almost a third (29%) also made a political commitment of revenues to support tax policy measures.

Revenue-neutral recycling versus revenue-raising expenditure

The World Bank, in a report titled Fiscal Policies for Development and Climate Action, explains that the use of environmental taxes is one of the most effective ways to combat climate change while simultaneously improving human welfare.

Referring to the use of environmental tax revenues, the World Bank distinguishes between revenue-neutral recycling and revenue-raising expenditure. The former comprises a reduction in labour and capital taxes, lump sum transfers to households, and output-based rebates to industry. The latter is for raising domestic resources to be used for public infrastructure investments, the provision of basic services, the funding of social protection programmes, and national debt reduction.

… the use of environmental taxes is one of the most effective ways to combat climate change while simultaneously improving human welfare.

Public preference

Over the past couple of years, various willingness-to-pay surveys have been conducted to gain a better understanding of the public’s acceptance of carbon pricing mechanisms. According to the findings of these surveys, the various carbon revenue uses can be divided into three categories: environmental, redistributive and other:

- Environmental revenue use refers to funds allocated to projects that reduce CO2 emissions or finance low-carbon energy sources, for example the funding of research and development of renewable energies, the purchase of foreign carbon credits, and the funding of technological innovation and energy efficiency.

- Redistributive revenues are allocated to the vulnerable to soften the regressive effects of carbon pricing, for example to low-income households and the elderly, or an equal share of revenue to each taxpayer.

- The ‘other’ category comprises revenue recycling (often referred to as ‘environmental tax reform’) through current tax reductions or allocation to the general budget.

Studies have shown that the public accepts carbon pricing more readily when revenues were recycled and not allocated to the government’s general budget, and when people trusted the political environment in their country. Societies are less willing to accept higher climate-related taxes when there is a lack of trust, or when corruption is suspected.

… the public accepts carbon pricing more readily when revenues were not allocated to the government’s general budget

A thematic approach

Another way of looking at revenue use classification is to adopt a thematic approach. Therefore, instead of being incorporated into a country’s general budget, carbon revenues can be allocated to fund-specific objectives. The World Bank’s themes in this context are (1) tax reform, (2) climate mitigation, (3) other development objectives, (4) prevention of carbon leakage, (5) assistance for affected stakeholders, and (6) debt reduction. These thematic classifications can be adjusted, depending on what the policymakers want to focus on.

Attributes of carbon tax revenue use options

Whichever modality is chosen, there are certain universal design characteristics or attributes that need to be taken into account as well.

The allocation of carbon tax revenues will reflect a specific government’s objectives and local context. As carbon tax revenue is mostly a supporting act for tax policy changes, it usually forms part of a larger tax reform. Carbon revenue use decisions should therefore be integrated with the overall fiscal framework.

A government’s fiscal policy objectives – for example to increase efficiency, promote long-term growth, enhance public acceptance of the carbon pricing mechanism and/or equitably distribute resources – can provide a fiscal framework for spending carbon revenues. The regulatory capacity and structures that are in place also contribute to the design and administration of carbon revenue spending.

No single carbon revenue use modality dominates from an economic or political viewpoint, as there are compromises across the various fiscal objectives. For example, designating carbon revenues to reduce national debt may be regarded as market efficient. However, it does not translate into political support. Consequently, policymakers need to find a balance between political practicability and public support factors on the one hand, and environmental effectiveness and reliable tax policy tenets on the other hand. It is suggested that decisions about carbon revenue use should always be made in alignment with fiscal policy objectives.

Societies are less willing to accept higher climate-related taxes when there is a lack of trust …

Suggesting a framework to support decision-making

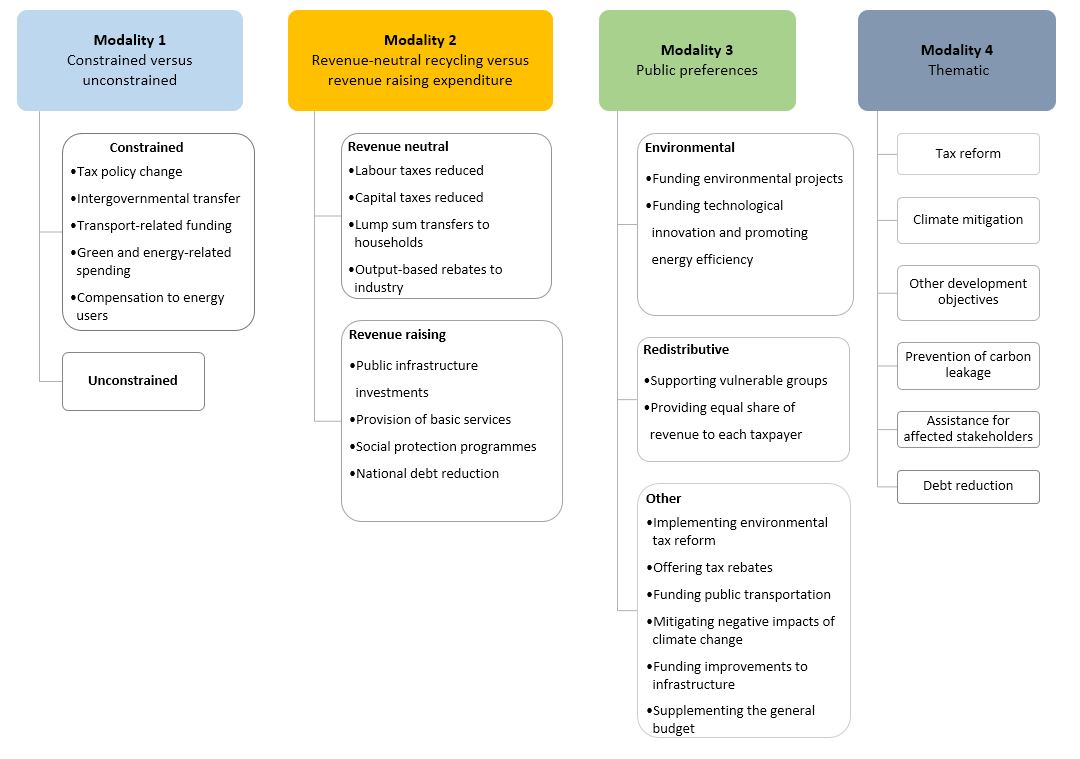

New tax law is usually met with opposition. The same applies to carbon tax. Yet, knowing how carbon tax revenues will be used will help to increase acceptance of this tax and will enhance policy certainty. Therefore, to help policymakers draft new or evaluate existing carbon tax policies, a classification framework for the use of carbon tax revenues has been proposed (see Figure 1). This framework has four modalities:

The first modality

delineates the unconstrained and constrained use of carbon revenues. The constrained use of carbon revenues can be split into political commitments and earmarking. In respect of constrained spending, this modality comprises the OECD’s six groupings, with ‘tax policy changes’ highlighted as the preferred choice for most countries.

The second modality

is based on the World Bank’s differentiation between revenue-neutral recycling and revenue-raising expenditure. Revenue recycling impacts households and industries in a direct manner through tax reductions, rebates and lump sum transfers. Revenue-raising expenditure results in more indirect, longer-term effects through enhanced social spending and public infrastructure investments.

The public’s willingness to pay carbon tax is largely influenced by how a government will spend this revenue. Consequently, the

third modality

is based on public preferences, and distinguishes between three categories of carbon revenue use, namely environmental, redistributive and other.

New tax is usually met with opposition. The same applies to carbon tax. Yet, knowing how carbon tax revenues will be used will help to increase acceptance of this tax and will enhance policy certainty.

The

fourth modality

entails the World Bank’s thematic approach for allocating carbon revenues to fund-specific objectives. The six themes comprise tax reform, climate mitigation, other development objectives, prevention of carbon leakage, assistance for affected stakeholders, and debt reduction.

The key policy insights based on this research are the following:

- Carbon pricing is the most cost-effective regulatory approach to reduce greenhouse gas emissions, and it is recognised as a significant contributor to government revenue.

- Carbon tax revenue use can be classified into four overarching modalities to cater for various policy design attributes.

- There is no dominating revenue use option from an economic or political viewpoint, owing to trade-offs across various fiscal policy objectives.

- Carbon taxes are elements of broader tax reform, and therefore revenue use options should be aligned with a jurisdiction’s broader fiscal policy charter.

To conclude, this simple and high-level classification framework for carbon tax revenue usage, as depicted in Figure 1, can be used by policymakers as a quick reference to identify the best carbon revenue use option when designing or refining carbon tax policies to meet their country’s climate targets and support economic development objectives. Once the policymakers have selected an appropriate modality, they can start with in-depth policy deliberations.

- Find the original article here: Steenkamp, L. (2021). A classification framework for carbon tax revenue use. Climate Policy 21(7) DOI: 10.1080/14693062.2021.1946381

- Dr Lee-Ann Steenkamp is an NRF-rated researcher and senior lecturer in Taxation and Management Accounting at the University of Stellenbosch Business School. She is also Head of USB’s Postgraduate Diploma in Financial Planning.