The Nationalisation of the SA Reserve Bank

the almost jealous protection of the autonomy of the country’s democratic institutions, such as the public protector, auditor-general, the judiciary, the media, and, of course, the SA Reserve Bank (SARB). Institutional soundness is generally accepted to be a necessary requirement for prosperity since institutions form an enabling environment for the creation of wealth. This is particularly important in encouraging collaboration between the public and private sectors in the pursuit of improved productivity. However, in the absence of strong institutions this alliance can become dysfunctional, with both sectors colluding in the pursuit of profit at the expense of consumers, voters, and taxpayers.

Unfortunately, the last few years have seen a real (or perceived) decline in the country’s institutional capacity and integrity. For instance, SA’s ranking for the institutions pillar in the World Economic Forum’s annual Global Competitiveness Report was a disappointing 76 in 2017-18. Rankings for various individual components of that pillar fell as follows from 2016-17 to 2017-18: Property rights – 29th to 56th; irregular payments and bribes – 53rd to 91st; judicial independence – 16th to 36th; transparency of government policy making – 44th to 74th; efficiency of legal framework in settling disputes- 9th to 31st; and efficiency of legal framework in challenging regulations – 10th to 36th. The 2017-2018 Report also indicates that the three most problematic factors for doing business in South Africa are corruption, crime and theft, and government instability. The impact of this institutional deterioration manifests in many ways, not least of which the downgrading of South Africa’s sovereign credit rating.

Throughout all of this, however, the SA Reserve Bank has stood firm and proud as a beacon of good governance, credibility, competence, and accountability. In fact, it is probably fair to suggest that the esteem in which the Bank is held helped prevent any further credit downgradings. It is therefore understandable that the intention to implement the ANC’s resolution that the SARB should be 100% owned by the state should send shivers down the spines of already nervous, risk-averse and cynical investors, business leaders and analysts.

The concerns are probably rooted in the fact that the SARB is one of only a handful of central banks that has private owners, and that this private ownership compels the Bank to act in a responsible fashion at all times. This, in turn, removes the temptation to, for instance, simply print money at the behest of the state (a la Zimbabwe). In the light of this, and given the already fragile state of the economy, any change in the ownership structure of the Bank may well be construed to be an unnecessary and damaging risk to the country’s longer-term economic prospects. It would probably also be interpreted as part of an ideological shift toward statism.

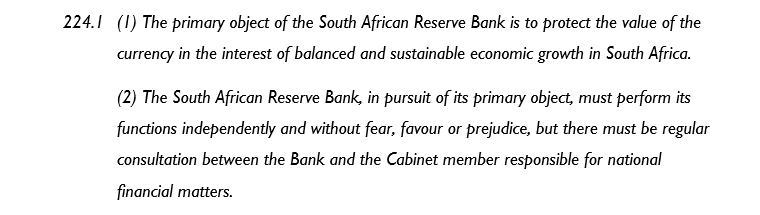

At this stage of the discourse it is fitting to remind ourselves of what the Constitution has to say about the primary object of the Reserve Bank. In Chapter 13:

At least two important non-negotiable (if we believe in the sacrosanctity of the Constitution) issues emerge:

First, the main mandate of the Bank is to protect the value of the currency – not to create jobs, or to reduce poverty, or to narrow the inequality gap. That said, the mandate recognizes the fact that, in the long term, price stability is an important co-creator of sustainable growth.

Secondly, regardless of who owns the Bank (private investors, or the state, or both), shareholders have very limited rights. They certainly play no role in determining or changing the mandate of the Bank; nor are they allowed to exert any influence on the decisions made by the Bank in executing their mandate, e.g., setting and adjusting the repo rate.

So, unless the Constitution is changed, nationalising the SARB will not change much at all. There is, of course, the prickly question of the assets held on the SARB’s balance sheet. In the event of nationalization, there is presumably a risk that these assets could be requisitioned by a debt-strapped government to bail out state-owned enterprises. On balance, common sense and reason should prevail to prevent this from becoming a major concern.

At this stage the weight of evidence suggests that the efficacy, independence, and cogent policy-making capacity of the SARB will not be unduly changed in the event of it being nationalised. It is, however, unfortunate that the issue should become part of the national debate at a time when the country has only just embarked on the first tentative and timorous steps towards restoring the integrity and capacity of its once-proud democratic institutions. One has to wonder whether the political posturing is really warranted.

Subscribe

Want to stay in touch with the Stellenbosch Business School community? Sign up and receive newsletters from our desk to your inbox.

SIGN UP