Elections 2019 and the impact on SA’s economy

Assume then that President Ramaphosa remains at the helm of the party and the country for the next 10 years, and that he slowly but surely instills a spirit of constitutionalism (as opposed to populism).

Can we now assume that economic growth will climb to 5% within the next year or two; that millions of new jobs will be created; that the “lights will stay on”; that most forms of crime will be of a petty nature; and that decent health care will be available and accessible to all? Of course not. With the best will in the world, one person (President Ramaphosa) cannot undo a decade of mismanagement and the warped allocation of scarce financial and human resources. Moreover, the predicament in which South African society in general, and the economy in particular finds itself can be attributed to a combination of external forces and internal, self-inflicted weaknesses.

Regarding external forces, the desired economic growth path of 6% per annum for a period of at least 20 years has to be achieved in a global economic environment that is less friendly and more volatile than 10 years ago. Indications are that world growth, especially in Europe, will remain sluggish for the foreseeable future, while trade tensions and the more robust oil price increase the risks for further contraction.

In some ways SA has “painted itself into a corner” with regard to its socio-economic lethargy.

For instance, the country, and its stakeholders, are living beyond their means in the following ways:

- Domestic expenditure exceeds domestic production.

- Government spending exceeds government revenue.

- Exports exceed imports.

- Household expenditure exceed household income.

- Investment demand exceeds savings supply.

The loss of fiscal discipline since 2008 is of particular concern. In the period between 1995 and 2008, a large measure of progress was recorded with regard to the country’s fiscal situation: government spending growth stabilised; government spending was re-prioritised; the country’s tax collection effort became increasingly efficient; the budget deficit was been narrowed (relative to GDP) to acceptable levels; and the public debt ratio was reduced. These improvements enabled the government to embark upon a programme of fiscal expansion to counteract recessionary conditions. However, the large rise in government debt since 2008 (currently approaching 60% of GDP), together with other fiscal developments, has attracted the attention of inter alia the well-known credit ratings agencies. The deterioration in South Africa’s fiscal prospects is largely due to government expenditure decisions over the last 10 years that are unrelated to the financial crisis. Of particular concern is the fact that about 30% of the rise in the spending-to-GDP ratio can be attributed to government wages; 15% to goods and services; and 11% to transfers. This is in addition to repeated rescue packages for inefficient state-owned enterprises. Moreover, the contraction in economic activity (and therefore the tax base of the economy), together with the political inexpedience of lowering government spending, is more than likely to result in relatively high budget deficits in the next few years, with a concomitant rise in the government debt to GDP ratio. Meanwhile, the budget will come under increasing pressure as a result of a rising debt servicing burden.

South African consumers are also living beyond their means. Household consumption expenditure on goods and services has exceeded household disposable income for more than a decade. As a consequence, the household debt-to-disposable income ratio has averaged just below 80% since 2006, compared to a long-term average of between 50% and 60% in the previous few decades (SARB, historical series). In addition, the ratio of household savings to disposable income has been negative for most of the period since since 2006; in 1992 it was as high as 6.1% (SARB, historical series).

The overarching and cross-cutting implication of the growing indebtedness of ‘SA (Pty) Ltd’ is that the country lives in perpetual hope that its various deficits will be financed by non-residents, at an affordable cost. Until about five years ago this outcome was generally achieved, as foreign savers found the country to be sufficiently attractive to warrant a meaningful investment in shares, bonds, plant, equipment and other forms of direct investment. But this might have been not so much a vote of confidence in South Africa, but rather a motion of no confidence in the short-term economic outlook then prevailing in the USA, Western Europe, and Japan. Today, investors are probably finding it more difficult to formulate good reasons for financing South Africa’s fiscal, household, foreign and savings deficits. On reflection, therefore, South Africa’s relatively robust economic growth performance during the first few years of the 2000s was largely driven by consumer and investment spending, which, in turn, was accommodated by rapidly expanding debt levels. The latter are not sustainable; in fact, as both the household and government sectors attempt to restore the integrity of their balance sheets, growth in these sectors is being curbed.

When all is said and done productivity is a prerequisite for international competitiveness and economic growth and development. Labour productivity is the most common measure of productivity, largely because labour costs constitute the largest share in the value of most products (in South Africa wages and salaries represent more than 50% of the cost of producing GDP). Capital productivity measures the output per unit of capital employed (fixed capital, inventions and land resources). Total factor productivity (TFP) measures the efficiency of all inputs to a production process; i.e., it not only labour or capital. Its level is therefore determined by how efficiently and intensely inputs are utilized in production. It plays a critical role in explaining economic fluctuations, economic growth and cross-country differences in per capita income. Factors contributing to TFP growth include innovation, the availability of skilled labour, the cost of conducting R&D, the availability of technology (and the efficiency with which technology is used), and the availability and ability of management to harmoniously and efficiently blend the available inputs.

The productivity of labour in South Africa has, at best, stagnated over the last 10 years, while remuneration growth has increased by more than 6% per annum. As a result the unit costs of labour have escalated to be almost three times higher today than at the beginning of the 21st century. All of this has occurred during a period of near-recessionary conditions and chronically high unemployment.

South Africa’s TFP performance over the last three decades has been disappointing when considered according to its own historical development, as well as when compared with other countries of a similar nature. There were 15 annual declines in the country’s TFP between 1990 and 2014. Consequently, the level of TFP in 2014 was 22.6% lower than in 1989 (computed from The Conference Board Total Economy Database; Adjasi, 2015).

The reasons for South Africa’s sluggish TFP performance can be attributed to, inter alia, low efficiencies in the use of labour and capital; a variety of challenges (including regulatory and financial barriers) that prevent businesses from maximizing their potential; and a low competitive base.

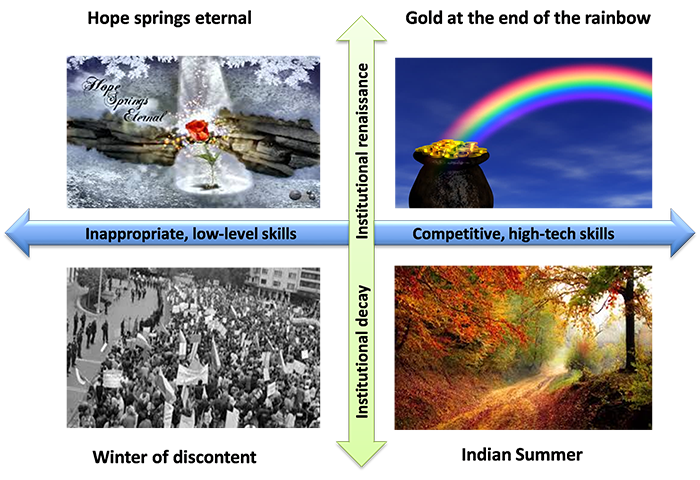

A key question, therefore, is whether we will we manage to generate sufficient appropriate skills to match the demands of employers? The OECD stated recently that the biggest challenge in South Africa is the unequal quality of school education, its low average level and the high drop-out rates.

Institutions matter a lot – generally, the prosperity of a country is closely correlated with its institutional quality. When institutions fail, trust is eroded and the stock of social capital depreciates, thereby compromising economic growth and development. Moreover, collaboration between the public and private sectors is a crucial co-creator of productivity growth; in the absence of strong institutions, however, the collaboration between the public and private sectors may become dysfunctional, with both sectors colluding in the pursuit of personal gain at the expense of consumers and taxpayers. Unfortunately, there is large body of both anecdotal and documented evidence suggesting that some of South Africa’s once-proud institutions and institutional values were dealt a cataclysmic blow during the almost decade-long leadership of former President Jacob Zuma. This was also accompanied by a warped allocation of financial and human resources. This is the legacy that President Ramaphosa has to contend with and repair. The crucial question in this regard is whether we will be able to restore and preserve the integrity, autonomy, and competence of our democratic institutions. Institutions establish constraints – both legal and informal (norms of behavior) – thereby determining the context in which individuals organise themselves and their economic activity. Moreover, institutions influence productivity, mainly through providing incentives and reducing uncertainties

Bearing in mind that all the forces and trends that drive socio-economic success are inter- and co-dependent, it can be argued that the two key uncertainties – the “make or break” issues that will determine the country’s future, are

- the generation of sufficient and appropriate skills; and

- the restoration of the capacity and integrity of our democratic institutions.

These two driving forces can be used to craft four scenarios of South Africa in, say, 2030, as depicted below.

The basic narrative of the “best case” (Gold at the end of the rainbow) and “worst case” Winter of discontent) scenarios can be presented as follows:

| Winter of discontent | Gold at the end of the rainbow |

|

|

It is rather unlikely that either of these extreme outcomes will transpire in exactly the way described above. The real, current question, therefore, is whether the future of South Africa will tilt towards the first, sanguine set of outcomes; or will we experience the tragic denouement portrayed in the second narrative.

A victorious ANC and its leader will not in and of themselves determine the country’s future. However, President Ramaphosa will hopefully use this window of opportunity to restore the aesthetic and moral fibre of society, so that normlessness, entitlement, and selfishness give way to ethical behaviour. He also needs to eradicate elitism, autocracy, and illegitimacy; and establish and entrench of a shared image of a desired future, with government playing a key visionary role, moulded by foresight and long-term planning,

At this crucial juncture of South Africa’s post-apartheid era, President Ramaphosa is arguably the only person with the ability and will to introduce and implement a plausible turnaround strategy. However, “one swallow does not make a summer”, and there is no quick fix that will yield immediate tangible results.

Subscribe

Want to stay in touch with the Stellenbosch Business School community? Sign up and receive newsletters from our desk to your inbox.

SIGN UP